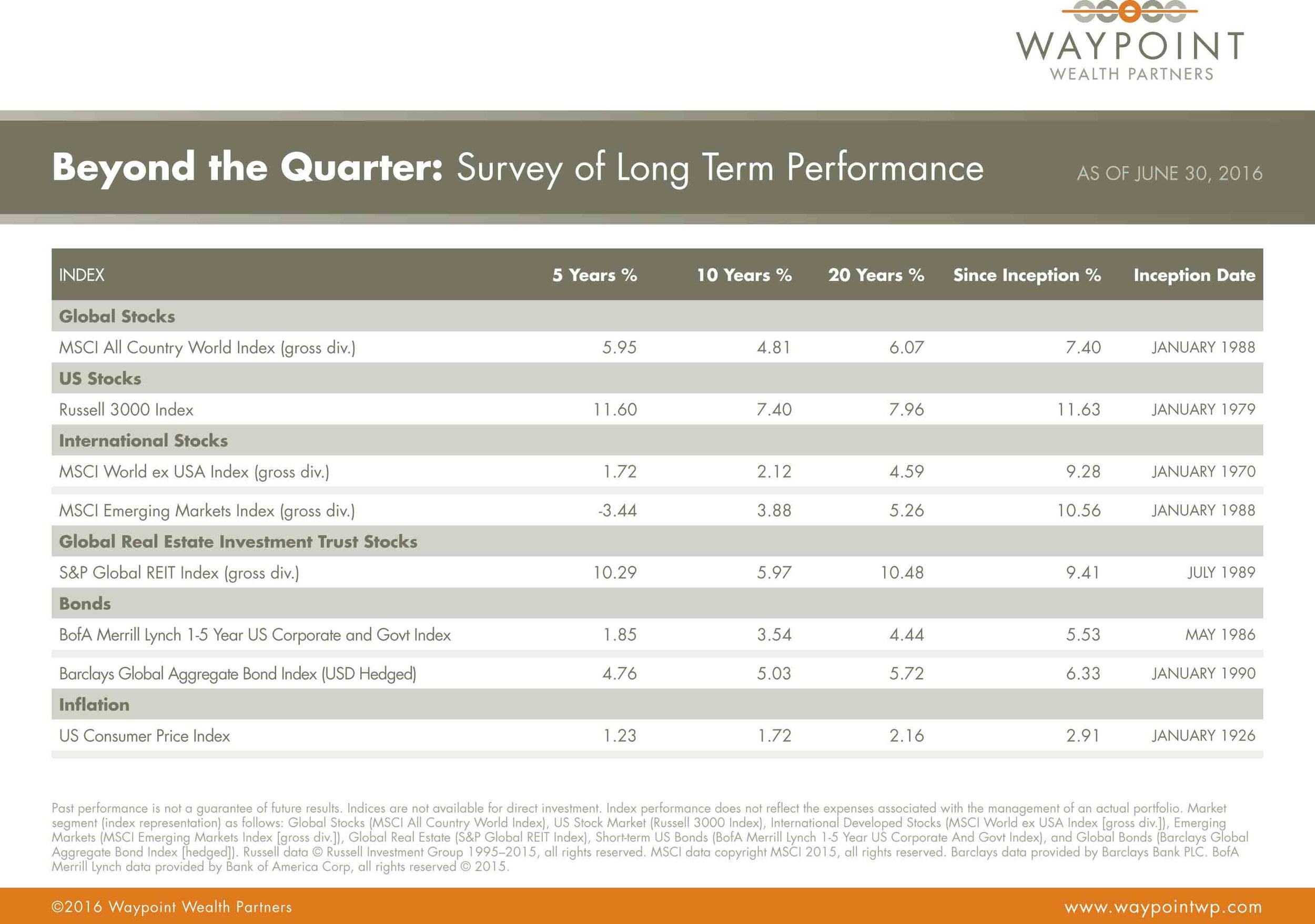

Both risky and safe-haven assets alike were on track to finish the quarter comfortably in positive territory until June 23rd when a majority of UK citizens voted to leave the European Union (EU). The so called Brexit rocked financial markets around the world. As a result, stock markets finished the quarter with marginally positive returns and in highly unstable fashion. The global economy continued on a sluggish path, which prompted further caution by central bankers and supported high quality fixed income assets.

BONDS

We have endured 7 years of intense focus on interest rates only to see them linger at record low levels year after year. The most recent quarter was no different. Bonds continued to defy expectations yet again as yields moved even lower. The increasingly uncertain economic environment created a favorable market environment for fixed income instruments and provided major central bankers with the data needed to remain supportive and maintain their stimulative policies. In Japan and parts of Europe rates moved further into negative territory while the yield on the benchmark 10 year US Treasury Note finished the quarter near record lows. As yields fell, the broad based US bond market returned 2.51%, high-quality short-term bonds earned 0.98% and international government bonds

finished the quarter 3.31% higher.

STOCKS

Equity markets spent the better part of the second quarter marching upwards only to be derailed at the eleventh hour by the UK’s decision to give up it’s EU membership. In the days leading up to the vote, markets rose steadily as investors became more confident that the UK would remain in the EU. As the news of the vote unfolded stocks around the globe tumbled. European equities were hit the hardest due to the heightened concern regarding the strength of the European bloc. While all equity markets did lose significant ground as a result of the UK referendum, US stocks managed to finish the quarter with a gain in the low single digits, supported by expectations that interest rates will continue to stay low for the near future. International developed markets were marginally negative due to their proximity to the effects of the Brexit. Emerging market stocks were just above zero but performance varied widely from country to country – Brazil was sharply positive as political instability waned while emerging European countries (Poland, Greece & the Czech Republic) underperformed.

ECONOMY

The US economy improved in the first two months after a weak start to the year. The strongest data point was a positive revision to first quarter GDP growth. The momentum was short-lived, especially on the unemployment front. The employment statistics for May showed the number of new jobs created surprisingly weakened, which dampened expectations for interest rate increases. Given the length of the US economic recovery we are likely reaching the later stages so it is not unexpected to see more volatile data points. Overall, economic growth remained around the 2% level and the US is still the strongest economy in the developed world. Across the Atlantic, Eurozone growth and inflation responded positively to stimulus measures early in the quarter but the unknown repercussions from the Brexit vote has complicated the path going forward. In Japan, the export led economy performed better than expectations but is also very exposed to fallout from Brexit. In the wake of the vote the Japanese Yen rallied since it holds the status of a safe-haven currency. Such movement does not help exporters as their goods become more expensive to the rest of the world. Emerging market economies saw relief from stabilizing commodity prices. However, demand for commodities has remained low relative to a year ago. Overall, the world’s economy remained stable but given where we are in the recovery and the complications created by Brexit, which will take years to unfold, the path forward is less clear.

Brexit: What Does It Mean?

On June 23, in a long-anticipated, widely reported referendum in the United Kingdom, voters chose to leave the European Union.

The debate over whether to stay or leave began not long after the United Kingdom joined the E.U. in 1973. It finally culminated in this decision—a momentous one for the United Kingdom, Europe, and beyond, given that the United Kingdom is a global financial center and the world’s fifth-largest economy. And the E.U., a union of 28 states, includes four of the world’s seven largest developed economies.

Near-term Ramifications

This vote will have a significant global economic impact. But because the referendum result itself is not a binding decision, it will take considerable time before that impact is fully felt. In the interim, uncertainty

will persist.

First, the result needs to be incorporated into an Act of Parliament in the United Kingdom. Under the terms of the Lisbon Treaty (part of the E.U.’s governing framework), the United Kingdom will then give formal notice to the E.U. After that, negotiations will begin on the actual exit terms. Those negotiations can span two years and may be extended further. The most immediate ramification, meanwhile, will be political change in the United Kingdom.

Implications for the U.K. Economy

Estimates of how Brexit will affect the U.K. economy range widely; some are positive, but the majority are negative. A key assumption in any Brexit scenario is what happens to trade agreements. The E.U. is the United Kingdom’s largest trading partner, receiving about half of all U.K. exports. Upon leaving the E.U., the United Kingdom will lose its automatic right to the favorable trade terms that E.U. membership bestows.

The International Monetary Fund (IMF), for example, projects that U.K. gross domestic product could drop more than 1% by 2021 under its most favorable scenario, which assumes the United Kingdom will retain access to the E.U. market. Under a less optimistic scenario, the IMF projects that GDP could drop more than 4%.

Concern about Brexit has already led businesses to put hiring and spending plans on hold, and it has decreased merger and acquisition activity. Less favorable trade terms could also discourage foreign investment in the United Kingdom by firms that might otherwise seek a U.K. presence to access European customers.

Immigration policy has been one of the major issues in the Brexit debate. Although it will still be possible after Brexit for E.U. citizens to work in the United Kingdom, such decisions are likely to rest with the U.K. government—in contrast to currently unrestricted access.

Suffice it to say that a whole host of new U.K. regulatory frameworks would need to be developed to conduct business and trade in a post-E.U. world.

Implications for Investors

Given that it may take several years for the specifics of Brexit to play out, and markets may be rattled as plans take shape, investors’ best protection is to hold a portfolio that is diversified across asset classes and regions. Although it is certainly worthwhile to keep abreast of global events such as the Brexit referendum, we caution investors against making tactical or short-term

changes to their portfolios.

Adapted from “Brexit: What does Vanguard Think?”, June, 2016 – www.vanguard.com. Vanguard Group, Inc. is an investment advisor registered with the Securities and Exchange Commission.